For decades, buying a house in the US meant spending around 5 times your annual income. And by last year, this ratio jumped above 7. This means the typical American family now needs to shell out more than 7 times their yearly earnings to afford an average single-family home.

The fact that “home prices have soared relative to incomes in a growing number of metro areas” has made homeownership a distant dream for many on low and moderate incomes. While taxes are a popular tool to try and cool the hot market, they are unlikely to be a silver bullet solution.

It has been closer to the end of the first quarter of this year, and the housing market stayed “predictable” that all of 2023’s headwinds continue to hold strong. Hiking property prices and a shrinking inventory are pushing anyone who are trying to afford a home far off the shore.

For aspiring homebuyers, the first question is how much of their annual income will be required to afford the mortgage payment on a particular home. There are ratios or equivalent measures that can help them assess this affordability, such as the house price-to-income ratio.

AN UNAFFORDABLE DREAM

Basically, the house price-to-income ratio (HIP ratio) boils down to how much house can you afford with your salary. It compares the typical cost of a home to the average household income in that area. This ratio is a key indicator of the overall housing market’s health, revealing if homes are becoming increasingly expensive and relative to incomes.

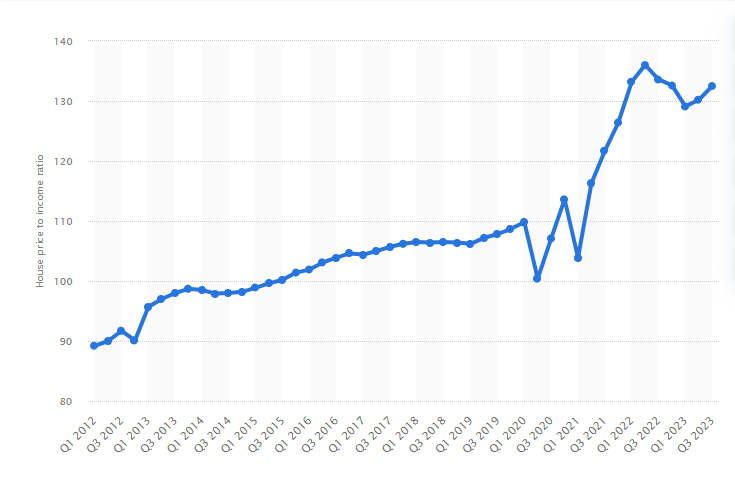

House price to income ratio in the United States from 1st quarter 2012 to 3rd quarter 2023 (source: Statista, updated Jan, 2024.)

According to Statista, affordability in the U.S. housing market took a hit in 2023. The house price-to-income ratio, a key measure for the housing development, rose after a brief dip in late 2022. This means homes are becoming much more inaccessible and expensive compared to what most Americans earn. One more thing should be noted from the chart is since 2015, house prices have outpaced income growth by almost a third.

A recent study from Harvard University also shed light on the worsening affordability situation in the housing market by showing home price-to-income ratio reaching records highs. To be specific, the 2022 median sale price for a single-family home in the U.S. was 5.6 times greater than the median household income, surpassing all previous records dating back to the early 1970s.

Looking at the present economic climate, it is clear how past economic shifts have strongly impacted the real estate industry. To combat the current recession and boost the economy, the Federal Reserve is expected to cut interest rates by the end of June. It, in turn, will make it cheaper for people to take out mortgages, encouraging more spending on homes.

Of course, FED’s act intends to make property purchase easier, but it also plays a major role in driving up house prices. Plus, a new generation of millennial homebuyers starts entering the market, “reaching the peak home-buying and family formation at this very moment” (Michael Hendrix). However, a lack of new construction and a rise in investors and corporations buying properties to rent out created a shortage of available homes. This limited supply, combined with high demand, continued to push prices upwards.

While a rising house-to-income ratio exposes affordability concerns, some argue that strategic tax policies targeting this ratio could help cool the market and curb the housing bubble. Not surprisingly, one common tax approach from the government is to implement property taxes.

YES, WE ALL KNOW ABOUT THE PROPERTY TAXES

Housing is a form of property and is therefore subject to tax. Not only in the US but in many countries, property taxes are also based on the value of the house itself. In these cases, if a house’s value exceeds a certain number, it will be subject to additional taxes. And as a matter of fact, property taxes have been implemented and recognized throughout the housing history.

At the same time, income generated from housing is taxed in two segments: rental income and capital gain. Owners can choose to combine this income with their other sources when filing taxes, or establish a legal entity to hold the property, depending on what best suits personal financial goals.

Rental income from owning property counts as regular income for taxes. As landlords pay taxes based on their income tax bracket, being aware of the 2024 bracket changes matters more than ever. Still, tax brackets are not all-or-nothing. As your income increases, you get taxed at different rates for different portions of your earnings.

Capital gains tax is like a fee on your investment profits. When you sell an investment for more than you bought it for, the difference is a capital gain. You will owe taxes on that gain, calculated by subtracting your original purchase price (and any buying fees) from the final selling price.

Property taxes, though controversial, can be structured to align with the “benefit principle” of public finance. This means those with more valuable property, often benefiting more from government services like infrastructure and schools, contribute a larger share. To certain extent, property value reflects the value of these services. Additionally, certain government investments, like high-performing schools, can even increase property values.

It is also important to think out loud that property taxes are a more neutral economic tool compared to other options. Since they target immobile assets like land and buildings, they’re less susceptible to tax competition and avoidance strategies. This contrasts with income taxes that might discourage work and investment, or other taxes that favor certain industries.

After all, property taxes can feel high, but they also discourage excessive house flipping. If local governments have to raise other taxes to make up for lower property tax revenue, it could hurt the economy overall. This is why a well-designed property tax system towards real estate can be a useful tool for managing housing markets.

LOOPHOLES DRAIN EFFECTIVENESS OF TAX POLICY

Let’s say that governments often try to slow down rising house prices by taxing them more, and at the end, avoid housing speculation. These efforts can be thwarted by the pass-through effect. Basically, if the tax burden remains within what buyers or renters are willing to pay, they simply pass it on down the line. This doesn’t stop the speculation cycle, as long as the belief persists that housing prices will continue to outpace inflation (CPI). In other words, as long as people expect to make more by buying and holding property, speculation remains a decade-long story.

There is a solution to address this speculation issue, even though it may not be a quick band-aid that can clear out the underlying problem. Reducing the net gain for investors by significantly increasing the capital gains tax. How’s so?

Consider a scenario where an investor flips a house for a 50% profit, but a 70% capital gains tax slashes their net profit to a meager 15%. Compared to other investments offering potentially higher returns with lower risk, house flipping becomes considerably less appealing because it dampens investors from entering the market solely for quick profits.

Soaring house prices are hitting big cities the hardest – these hubs of jobs, finance, and politics. But there’s a catch: these same cities have limited land, which is shrinking fast. With rising land, materials, and labor costs, building affordable housing becomes less profitable for investors. Worse as it may seem, this shift in economics makes luxury projects more attractive, pushing affordable options out of the picture.

Getting rid of the housing speculation in major cities requires the governments to focus on the core idea of: houses should be, primarily and solely, made to live, not for the sufring profits. Therefore, a two-pronged approach is needed: restrictions and incentives. It involves a steeper upfront cost for buying high-end homes. These funds could then be redirected to support the development of affordable housing projects, making homeownership a pleasant to the ears of low to middle income residents.

Another key element to restrict the speculation, as mentioned above, is a well-fit capital gains tax. The tax rate should be high enough to deter short-term flipping, but not to an extent that it discourages long-term investment. Certain countries have implemented tiered capital gains taxes, with higher rates for properties held for a shorter period and lower rates for primary residences.

Yet, tax policies alone might not be enough to break the speculation chain when housing supply is limited. Singapore offers a valuable case study. Their approach goes beyond just taxes. Reportedly, they actively manage the housing supply, provide financial support for first-time buyers, and have established a renowned system like the Housing and Development Board (HDB) with its Central Savings (CPF) program.

Taking everything into account, taming housing speculation goes beyond just tax tweaks. A successful strategy would be multi-faceted, addressing affordability for the middle class through targeted programs, boosting housing availability, ensuring clear market information, and exploring innovative ways to utilize long-term savings for mortgage payments.

Reece Almond

Disclaimer: The blog articles are intended for educational and informational purposes only. This article draws in part on the research of Professor Vo Dinh Tri. Nothing in the content is designed to be legal or financial advice.