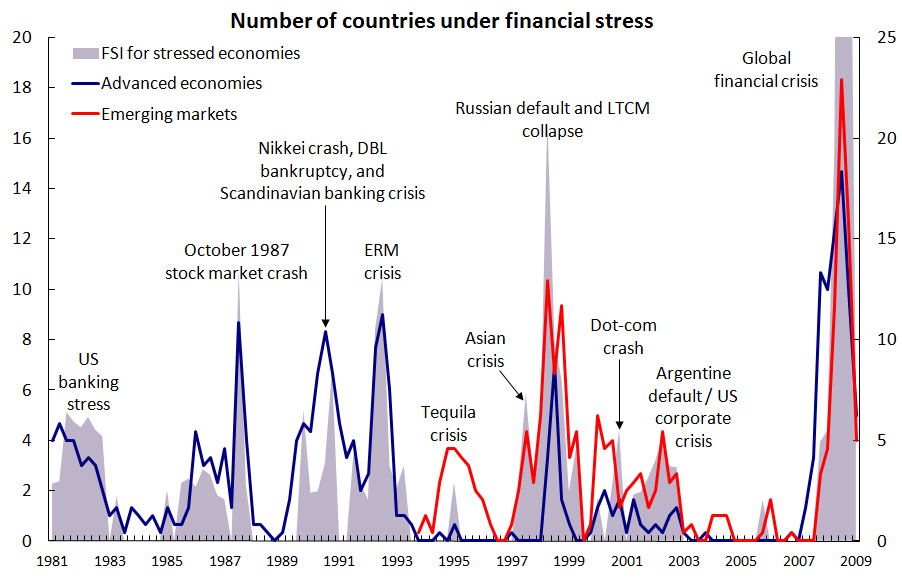

| While the citizens wonder how and when the current global debt crisis began, most wonder what is the root of it and if this root planted the seeds for the most significant financial catastrophe since the Great Depression is the US housing bubble, which bloated in 2007. |

SRI LANKA AND ITS STORY

The New York Times reports that Sri Lanka used to be an ideal choice for many expats looking for a secondary home valued up to millions of dollars. The trend of real estate speculation exploded in this country when villas on the beach or in popular tourist locations became a magnet for the rich.

Instead of investing in manufacturing businesses to push the economy forward, Sri Lanka went all in its tourism and the real estate speculation market. Most of the selling items were not originally from the nation itself, but marked as “made in” from a particular country. As inflation spiraled out of control and the banking system collapsed, Sri Lanka’s economy fell into anarchy when it defaulted on its debt for the first time in May 2022.

It is not uncommon to hear people rushing to speculate on real estate and causing a market bubble that puts the financial system at risk. Whereas Sri Lanka is a cautionary tale against relying too much on real estate and overlooking other industrial industries, the 2000s housing crisis in America is a glaring picture of what a true housing bubble looks like. The greatest economy in the world soon recovered, but the rest of the world is still crawling to bounce back even after a decade of post-recession.

Now that property bills are rising and changing across the board. In the US, prices were 50% higher between 2012 and 2019 and this is the third-largest housing boom in history. The spillover effect of post-pandemic only thrilled buyers’ demand but froze the supply in the market, causing prices to drive up constantly. Home prices are much higher than they were at their peak in 2007, when the housing bubble burst. Following the peak, the market showed signs of meltdown, before dropping by 60% and bottoming out in 2012.

Another bubble, one that will be as damaging as the housing bubble of the 2000s, is something many worries about has already arisen.

HOW BUBBLES STAY AFLOAT

The term “bubble” is when asset prices, including those of stocks and homes, diverge from their fundamentals.

The fundamentals are the actual value of an asset. This value of a property includes factors like its adjacency to locations with high job potential, quality healthcare and educational options, and a variety of lifestyle amenities. Supply and demand for housing in a particular area shall also prompt the property’s value. If there are not enough homes available for people to reside in where they desire, the value of those properties will gradually climb up. In short, the housing bubble refers to a situation in which the price of a commodity or asset is way higher than its true value.

Since the middle of the 1990s, housing bubbles in America have been a sweeping storm of speculation, together with US stock bubbles. People who made a heavy fortune from stocks started splashing their money on bigger, fancier homes. This increased demand drove up housing prices, only encouraging more people to jump in.

Investors lost faith only briefly after the US stock market bubble cracked in 2002, investors lost faith. Millions dashed to real estate as a safe haven, causing the housing bubble to swell even more significantly. This price race greatly impacted on supply, leading to the construction of new properties to go through the roof. By 2002, house ownership had increased by almost 25% compared to the pre-bubble, but vacancy rates had also risen to nearly record highs, exceeding 9%. The cumulative value of secondary housing credits then amounted up to $600 billion.

In 2007, the housing bubble began to shatter when prices could no longer keep up with the supply created by the construction boom. US home prices peaked in the middle of 2007, then slid down. The number of mortgage foreclosures considerably increased between 2006 and 2007, with mortgage assets suffering a sharp decline in value and the balance assets of lenders falling low.

WHAT’S INSIDE OF A BUBBLE

There has been a decades-long economic debate about why home values move away from their actual value. Economists Gabriel Chodorow-Reich, Adam M. Guren, and Timothy J. McQuade marked some insights on home prices in “The 2000s Housing Cycle With 2020 Hindsight: A Neo-Kindlebergerian View” study. They found that factors like job growth and amenities firmly increase market housing demand. They also evaluated how challenging it would be to refill the supply of new homes in specific locations to meet soaring demand.

These factors are claimed to be responsible for the most long-term surges in home prices in certain areas. Additionally, the study discovered that these elements explain why some markets see the most robust booms, property sales, and substantial recoveries. According to NPR, a well-known American nonprofit media organization, dominant housing markets throughout decades are mostly reported to be “superstar” cities. The highest long-term growth rates are observed in superstar cities with limited supply, numerous expanding industries, and stable employment, such as San Francisco, Seattle, San Diego, and Boston, suggesting that this was a fundamentals-driven cycle.

But if exorbitant prices are a testament to their importance, why do their bubbles appear more fragile than anywhere else?

To explain this, Chodorow-Reich and his colleagues adopted a theory from “Manias, Panics, and Crashes”, one of the best works by financial master Charles Kindleberger. The book presents a thorough history of financial crises, from the financial crisis in the Roman Empire, the Dutch bulb market bubble to the dot-com boom of the late 1990s. “The main thing we draw from that book is the idea that these boom-bust cycles start with some change in fundamentals,” Chodorow-Reich says.

Kindleberger’s theory states that when investors were over-excited about dramatic economic changes, they began to borrow wildly from banks to invest more in property and racked up debt. But when reality finally set in and prices started to fall, they were left holding the empty bag. Unable to pay off loans, they accidentally triggered a financial crisis that would echo as a repeated cycle throughout history.

Chodorow-Reich and his colleagues found that the US housing bubble incident followed an exact pattern to the speculative cycle,leading cities like San Francisco, New York, Boston, and other megacities to reshape what it means to live. Technology developed rapidly. Investing performed vigorously. Other industries also experienced noticeable growth. They become desirable locations to live, attracting millions of people looking for so-called bouncy living standards. Meanwhile, there weren’t enough homes available to meet the increased demand.

“Those fundamentals made prices rise — but then homebuyers got over-optimistic about that,” Chodorow-Reich supposed. When house prices continued to hike, homebuyers became unduly optimistic about their never-ending surge. This belief led to a frenzy of housing speculation, as people bought homes not to live in, but to flip for a profit, which also means buyers soon stray from the actual value of an estate. Given how prices fluctuate, a mortgage bomb could be found. Many homeowners were not able to stand still. They owned more on their mortgage than the value of their houses once property value showed signs of decline. When combined with a more widespread recession that destroyed employment and harmed earnings, it also led to a wave of foreclosures.

An abundance of foreclosed properties flooded the market, forcing prices so low that they deviated from their fundamentals. But it also built the foundation for the rebound. It explains why the US went through another housing bubble in 2012 after the backlog of foreclosed homes had been bought.

BUBBLES TROUBLE, BUBBLES POP

Truth is, bubbles will always pop. And when they pop, we see the world exactly as it is: bared and uncovered. This is when lurking nightmares emerge.

The US housing bubble burst soon turned into a global phenomenon as home prices had swiftly fallen to the bottom. US real estate securities plunged without stopping, causing significant damage to worldwide financial institutions.

Higher risk of credit scarcity formed, and the financial crisis hit harder when a series of US top names collapsed. New Century Financial Corporation filed for bankruptcy in August 2007. Bear Steams crashed crashed, before it was sold to JP Morgan Chase in March 2008. Five months later, Lehman Brothers, one of the oldest and largest investment banks in the US toppled, which until these days, is seen as a seminal and unforgettable moment in banking history. Bank of America boldly acquired Merrill Lynch – the third-largest investment in all-stock transactions. The US government took over AIG, the world’s biggest insurer, in a $85 billion bailout. Credit hunger affected production, the unemployment rate widened, and households seized their spendings, causing many businesses to go bankrupt.

The situation was so depressing that President George W. Bush and Chairman Ben Bernanke of the US Federal Reserve made announcements meant to stop homeowners who could not afford high-risk mortgages to soothe the financial market turbulence brought on by the credit crisis. In 2008 alone, the US spent up to $900 billion to bail out the real estate market, and countless financial institutions could not stop declaring bankruptcy.

The United States Senate even enacted the Emergency Economic Stabilization Act of 2008, giving the Treasury Secretary the authority to use $700 billion to salvage the US economy by repurchasing soured loans, particularly credits with real estate-backed debt.

Housing bubbles are nothing new, and this is not the first real estate descent to cross borders. America and other nations have already gone through similar downturns. However, because of the connections across financial markets, this 2000s crisis resonated significantly louder. Layers of underlying causes are still being broken down; one of them a complex interplay between value and liquidity in the US banking system triggered the financial crisis.

Experts confirmed the recession could eventually turn into a total collapse, and some countries faced much more painful monetary adjustments than the United States itself. By the end of October 2008, the currency crisis expanded as investors moved their sizable capitals to stronger currencies like the yen and Swiss franc. These currencies’ values were forced to rise, which made it harder for these nations to export their products. It deranged emerging economies and pressed them to request help from the IMF.

The nightmare of the global bust ended in June 2009. It caused US administrations to reassess the regulations of banking and credit sectors. Dreadfully, it took the US ten years to overcome the nightmare and thrive over the housing bubble’s shadow. Even when the American Recovery and Reinvestment Act of 2009 was made public, the US under Barack Obama’s administration faced challenges in implementing economic stimulus measures to recover from the Great Recession.

BRIDGES BURNT, LESSONS LEARNED

Half of 2023 has passed and the world’s economy is forecasted to undergo many more dramatic changes. Spillover effects from post-pandemic and ongoing monetary policy changes have left the real estate market in despair. According to Bloomberg Economics, property prices have surged unbelievably since the 2008 recessionary shock.

A cocktail made of an eclectic mix of ‘ingredients’ is driving home prices to unprecedented levels, economist Niraj Shah wrote in the report. Those ingredients include hiking interest rates, available savings deposited in the bank, limited housing stock and expectations of a strong recovery in the global economy, the need for additional space among remote workers and tax incentives for homebuyers.

Many worry about another housing crash similar to the one 10 years ago. But Niraj Shah believes the current real estate market is now different, with a low possibility of a housing bubble crisis despite mounting risk signs.

Spring is typically the peak season for home sales in the US, but since the FED decided to raise interest rates in early 2022, the housing market fell into a deep freeze. Rising interest rates make it harder to borrow money, which has led to a dip in the number of homes being bought and sold.

According to the National Association of Realtors (NAR), home sales in March fell 22% compared to2022. “We are in a real gridlock situation,” said Robert Frick, corporate economist at the Navy Federal Credit Union. “It’s going to be a tortuous process to unfreeze the market and take a long time to get back to a normal supply-and-demand situation.”. A forecast by KPMG LLP on the US housing market shows that sales will plunge by roughly 23% by the end of 2023 compared to 2022, marking the most significant drop since 2007.

Leading real estate consulting firm Knight Frank published its wealth report for the first quarter of 2023, in which high-end real estate prices worldwide recorded the first decline since the 2008 global financial crisis. House price index in 46 major cities decreased by 0.4% compared to 2022. The most severe decline in the property market was in New Zealand, where luxury home prices in Wellington, Auckland, and Christchurch all fell by double digits.

The real estate market won’t crash, at least for now. But it will undoubtedly cool off in the near future. The current housing market seems to be more into screening out risky issues, notably corporate bonds. Lessons from past crises alert governments to tighten lending decrees. Nations around the world have also solidified their macroeconomic safety nets towards potential threats. That being said, business owners should restructure operations by cutting off prolix projects in order to reduce debt and gain better financial value.

Unavoidable as it is, the market might become even more unstable if home prices continue to soar. As the lending rate ascends and broader measures are put in place to secure global financial stability, the housing market has yet to cross many abrupt tests.

Again, there are significant difficulties in the real estate market. Just like Adam Tooze, the famed English economist historian and professor of Columbia University, New York said: it’s a big recession risk!

Reece Almond

Disclaimer: The blog articles are intended for educational and informational purposes only. Nothing in the content is designed to be legal or financial advice.