As homeownership becomes increasingly unattainable for many, rent demand and costs see no sign of cooling off. This is a hurdle for renters but an opportunity for investors seeking to diversify their portfolios through rental properties.

Beyond the classic debate of rentals versus REITs, the impact of rent control policies, especially in Illinois and California, adds another layer of intricacy to investment decisions.

Definitions and how these types of investment work

Rentals: Investors typically acquire property, either through purchase or rental, renovate it, and then lease it out at a premium to generate income. Common rental properties include single-family or multifamily real estate.

The goal is for your rental income to outpace the costs of owning the property. These costs include your mortgage, taxes, insurance, and upkeep. The money left over after covering these expenses is your profit, or cash flow.

REITs (real estate investment trusts): This is a company that owns or finances a portfolio of properties. Each REIT has its own investment strategy and property mix.

By investing in REIT shares, individuals can share in the profits generated from these properties. To qualify as a REIT, a company must distribute at least 90% of its taxable income to shareholders in the form of dividends.

Unlike owning a rental property, where you have full control, investing in a REIT means giving up day-to-day management decisions. You don’t choose which properties the REIT buys or sells, or how they’re managed. These decisions are made by fund managers.

Why rentals?

Hands-on control. You dictate property selection, deal terms, rental rates, and renovations, providing maximum flexibility. It’s you who decide and do it all by yourself.

Value appreciation potential. Unlike REITs, which are subject to SEC regulations and management fees, rental properties allow for direct reinvestment of income. Property value can be boosted through improvements like ADU additions, ultimately increasing rental returns.

Hedge against stock market fragility. Unlike public REITs, real estate often moves on its own. So, let’s say the stock market crashes, owning a property for rent canbe a safety net for your portfolio. For example, during the 2008 financial crisis, while stocks dropped around 30% in market value, rental properties continued to generate income and thrived above the market returns.

Maximize investment with leverage. Rentals offer a very beneficial perk: you can borrow up to 80% of a property’s value, meaning a smaller down payment, compared to REITs’ limited debt options with a stricter financing limits, typically below 40%. This allows for larger investments and amplified returns on equity. For example, a $30,000 down payment can purchase a $120,000 property, capturing its full appreciation potential.

Tax benefits: Landlords have more chances to reduce their tax burden. Deductions often include mortgage interest, property taxes, insurance, repairs, and even a portion of the property’s value over nearly 30 years. A potential for 1031 exchange is also a plus. Landlords can postpone capital gains taxes by reinvesting sale proceeds in another property through a 1031 exchange.

Why REITs?

Lower cost. By dividing ownership into shares, you can invest in REITs with just a few dollars each. And most of the time, public non-traded REITs require lower initial investments compared to privately held REITs, lowering the entry barrier for new investors.

Good liquidity. Compared to physical rental properties, REIT shares can be sold quickly and easily. REITs allow investors to access their money whenever they need it, unlike rental properties which require a significant upfront investment and tie up funds for years.

Pass-through taxation. Because REITs pass most of their income directly to shareholders, they aren’t taxed as a company. Moreover, REIT investors enjoy a 20% tax deduction on loan interest and rental income, effective since 2018. All of this means investors only pay taxes on their personal income from the REIT, potentially leading to higher overall returns.

Portfolio diversification. REITs offer exposure to a wide range of real estate assets. With 200+ REITs available in the US, investors can access both residential and commercial properties. Each REIT owns numerous properties across various types, such as apartments, single-family homes, and commercial buildings. This broad ownership structure helps mitigate risk, as the performance of one property is less likely to significantly impact the overall investment.

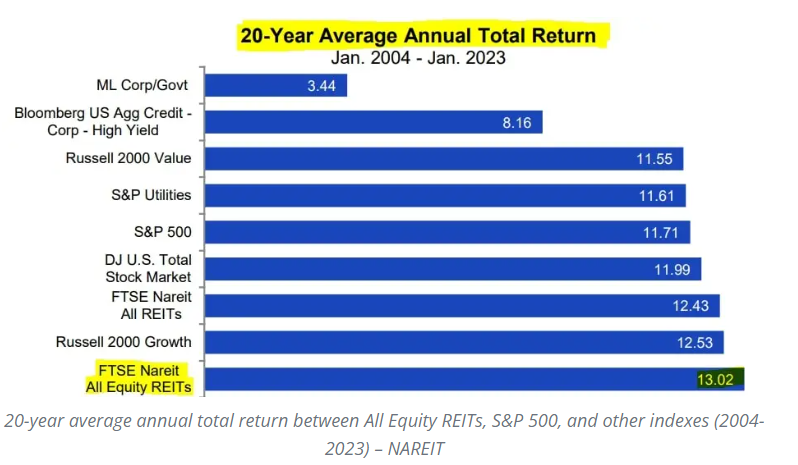

High short-term returns.

REITs have consistently outperformed the S&P 500 and growth stocks, delivering an average annual return of 13% over the past 20 years. According to Jussi Askola, president of Leonberg Capital, some REIT sectors, like self-storage, have significantly outperformed the overall REIT average, delivering around 19% annual returns over the past three decades.

Prefer a hands-off investment strategy? REITs might be the perfect fit. Looking for more control and potential tax advantages? Rental properties could be your answer.

For many investors, a blend of both offers the best of both worlds. Diversification is key to weathering market storms, so consider whether REITs, rental properties, or a combination align with your financial goals and investment style.

Especially with the rental market in flux and the heat of 2024 election approaching, understanding the hot-button impact on your real estate investments is crucial. Therefore, we’ve gathered key pointers regarding the rent control politics, so you can gain more in-depth insights to move forward with your investment strategies.

The rent control politics

It can be said that “rent control has nothing to do with housing at all, but is really an effort to gain political power, and control of private property with the false promise to people that somehow they will get to choose how much they’ll pay for rent.”, said Roger Valdez, director of the Center for Housing Economics.

According to Forbes and National Review, here are some highlights about what has been happening with the rent control politics across the US:

Rent control is really one instance of a price control, a legal limit on what a seller can charge a buyer. This intervention in the market is as old as civilization itself.

The truth is that it isn’t the consumer that controls rent, but City Hall, the same people who can’t figure out how to fill potholes, resolve tensions between police and people of color, or process building permits. Landlords there are suing an unelected junta (something called the Rent Governance Board) that sets price, based in part on the fact that the prices don’t reflect the actual costs of managing a functioning apartment building.

The problem with rents that don’t reflect anything other than an arbitrary determination by a government board extends to cost management. In New York, landlords are suing the Rent Governance Board (RBG) in part because rent control does not allow properties to keep up with costs.

If history tells us anything, this isn’t a battle that will be successful just with good facts; defenders of market principles will need lawyers and organizers to offset the other side’s alluring but false promise of a “pay what you will” rental economy and the end of private rental property.

Just yesterday, President Biden announced new actions to lower housing costs, including calling on Congress to pass legislation giving corporate landlords a choice to either cap rent increases on existing units at 5% or risk losing current valuable federal tax breaks. This would apply to landlords with over 50 units in their portfolio, covering more than 20 million units across the country. The policy is a bridge to rents stabilizing as President Biden’s plan to build more takes hold. The administration looks forward to working with Congress to ensure renters are protected and corporate landlords comply with the intent of this proposal.

The president’s proposal falls short in a formal sense of rent control, as it merely denies certain corporate landlords of existing properties a tax “break” if they increase rent by more than that arbitrary five percent. The Wall Street Journal weighs in, noting that the White House’s rent-control ultimatum won’t discourage new housing investment because it would apply only to existing units. Developers will rightly anticipate that the policy will eventually be extended to newer units, which will factor into their investment calculus. Reducing the return on completed projects also reduces the capital available to invest in new ones.

The government has spent five years waging a war on landlords, leading to many of them pulling out of the market, sending prices soaring, and creating intense supply shortages. New York City is in the midst of a housing crunch, and “ghost apartments,” empty rent-controlled units that are not in any rentable condition, are contributing to it. Rent control messes with the market pricing mechanism, with predictably destructive consequences, and creates a powerful constituency of renters who will resist anything but minor changes.

Economic theory grants us predictions about these regulations. Tenancy rent control and contract length regulations burden landlords with more risk of obtaining submarket rents within tenancies and being stuck for three years with troublesome renters. On the margin, this makes it more lucrative to sell properties for owner occupation, list on excluded short-term rental sites like AirBnB, or even just leave properties empty. By reducing the supply of traditional rental homes, this raises the average level of rent, even if the growth of rent is capped within minimum length tenancy contracts.

An environment of high inflation worsens these risks for landlords. With surging prices, it makes sense to change rent levels more regularly. This allows tenants and landlords to find contract provisions to make sure rents both reflect market realities and tenants’ ability to pay (as wage growth often lags inflation). Yet these regulations only allowed rent adjustments once per year (or twice from October 2023). High and volatile inflation thus interacts with these regulations to raise rent risk and vacancy risk (given the sharp jumps in rents). Landlords might therefore like to hedge against inflation by charging in another currency, like dollars. But this was prohibited too.