Contrary to popular belief that you need a mountain of cash to start investing in real estate, you don’t. In fact, capital-free real estate strategies are now one of the most popular investment methods.

IS IT TRUE?

To put it precisely, no. But it is true you do not need your own money to invest in real estate. When you find your dream property but it’s a bit out of your current budget, that’s where mortgages come in, meaning you can use bank capital through borrowing for investing in real estate.

With a real estate mortgage, you borrow a specific amount of money from the bank by using your assets as security. Assets can be land, homes, buildings, and other items affixed to real estate. The assets you use as collateral must be legally yours, or you need the owner’s permission if it belongs to someone else (normally a close family member).

Typical uses for loans include business loans (used by businesses), and consumer loans (popular with unsecured loans, due to modest loan amounts and rapid procedures), real estate loans and construction loans. Loan procedures vary depending on which purposes the loan is being used for. Apart from banks, consider credit unions as your loan source because they frequently offer competitive rates or special programs for members. You can also work with a real estate agent in which they guide you through the document’s preparation.

Banks typically lend you 70-90% of the property’s value. So, for a $200,000 house, you could borrow around $140,000-$180,000. To make sure you can actually repay the loan, banks will set a limit on your monthly payments. This limit is mostly around 50% of your income, ensuring you have enough left for other essentials. While the bank might be okay with 50% of your income going towards the loan, for your own financial security, it’s best to keep it at 30% or less. Think of it as leaving more room in your budget for unexpected expenses or future save-up.

A loan duration could range from 5 to 30 years. To ease the financial strain, you should extend the loan duration as much as you can or spread the loans out over the years. But here’s the catch: a longer loan means more interest charged overall. Once you’ve enjoyed those lower monthly payments for a while (usually 4 to 5 years when prepayment fees go away), you can turbocharge your repayment by adding some extra oomph to your monthly payments.

Of course, choosing the right bank is like picking the perfect pastry – consider all the ingredients, not just the sweetness. Apart from interest rates, there are other factors to consider. One of them is the bank size. Think of big banks like giant cake factories – they can get cheaper ingredients (deposits), so their baked goods (loans) might cost less too. State-owned and foreign banks often fall into this category. In addition, remember to do research on additional fees (like insurance costs) and loan conditions (like prepayment penalties).

WHAT ARE THE CONDITIONS?

Legally, there is not much difference between American citizens and foreign citizens who wish to own a home in the United States. The easiest way is paying upfront. But if you need a loan to purchase a property in the US, here are certain requirements you need to qualify:

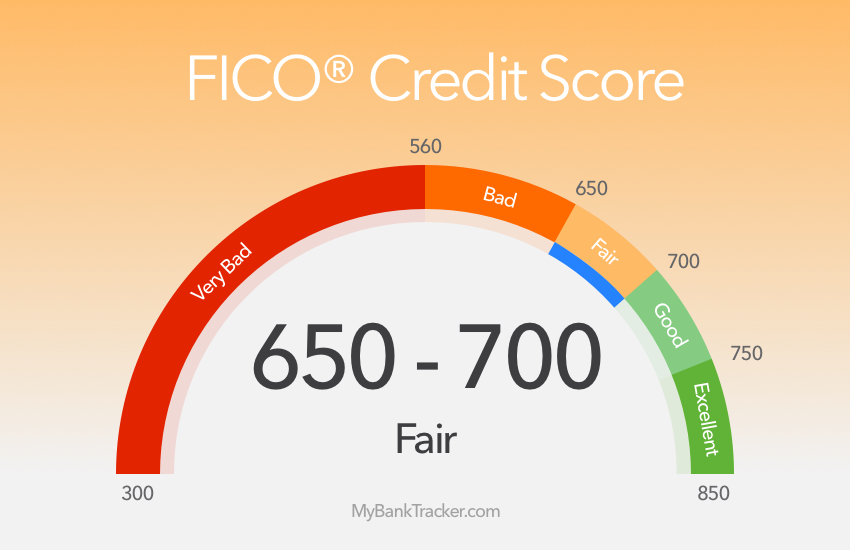

- Have a credit score of 720 points or above

- Have lived in the US for at least two years

- Pay 20% of the house worth up front

- Have a valid Social Security number (SSN)

- Have at least two years of job experience in the US

- Have a current source of income in the US and expect it to be sustained for at least three years.

Getting a green card from the US can make it easier for non-American citizens to get financing to buy real estate in the US. In fact, foreign nationals living in the US may be eligible for government-backed loans. This type of loan is subsidized by the US government to protect borrowers from default. Federal Housing Administration (FHA) loans, which are intended especially for those with green cards or temporary residency permits, are among the most well-known.

WHAT IS THE PROCESS?

Applying for a mortgage requires certain documents, such as proof of income through tax returns and a 2-month bank statement history. This is standard practice, but lenders might have additional requests, so checking with them directly is a necessary move for any borrower.

Home loan documents in the US typically includes:

- Legal residence documents and visas

- Loan application form (according to bank form in the US)

- Documents proving tax payment and history of working and trading in the US for the most recent 2 years

- Bank statements for at least 2 months

- Documents/evidence proving that the borrower will continue to live and work in the US within the next 3 years

- Documents proving the borrower’s income in the US: labor contract, salary statement, salary confirmation.

- If your source of income comes from business, American home loan borrowers need to provide a business registration license, financial statements, revenue reports for the most recent 6 months

Loan process to buy real estate in the US typically includes:

- Provide loan documents to banks/lending organizations: foreigners need to prepare all necessary procedures and documents to be able to borrow capital from banks or lending organizations.

- Document appraisal: based on loan application information, banks or lending institutions will conduct an appraisal process to check credit history, residence documents and legal visas in the US, and appraise place of residence, place of work/ business, and request an appraisal to determine the value of the house.

- Loan approval: if the application is eligible for a loan, the bank/lending organization will send the borrower a loan approval notice, grant credit and conduct disbursement-related procedures.

- Disbursement: once the home purchase contract is notarized, the loan will be disbursed.

WHAT QUESTIONS SHOULD YOU RAISE?

Talk to your advisor and raise a few straight, clear and simple questions before you take out a mortgage. This makes it easier for borrowers unfamiliar with the loan process to understand what information they need. You can ask:

- “How long will the whole mortgage process take?”

- “Will you be my main guide all the way or will someone else handle later steps?”

- “Which parts can I do online and what needs to be done in person, like getting the house valued or signing the final papers?”

- “For how long does the interest rate offer hold? If something delays things on my end, will I have to pay extra to keep it valid?”

If you are working with a broker,

- Check if they’ve considered other lenders: “How many offers did you compare, and why do you think this one is the best fit for me?”

- Make sure you’re clear on costs before accepting a loan. Ask your broker: “What fees are involved, and who pays them? Is it me, the lender, or both of us?”

WHAT DOES THE EXPERTS SAY?

Experts’ help is more than needed while navigating the loan maze, especially for first-time homebuyers. Their extra guidance can equip you with the details you need to make informed decisions.

First-time buyers face a lot of unknowns, says Joel Gurman, president of Rocket Mortgage, regional vice president of mortgage banking. Money and location are the big two. Having a rough idea of your desired area saves time and keeps you focused on finding homes that fit your budget within the location.

Be financially ready

In the US, buying a house with a low down payment is possible, with US institutions willing to lend up to 85–90% of the home’s worth. Government-backed loans like FHA and USDA can even require as little as 3.5% or 0% down. However, if you put down less than 20%, you are likely pay “loan insurance,” which adds about 1% to your yearly interest rate. Also, these loans do not cover home repairs or closing costs.

And your credit score matters too. Higher scores mean better loan rates and higher loan amounts. Aim for a credit score above 640 (the average) and a debt-to-income ratio below 36%. This ratio tells lenders how much of your income goes towards debts, ensuring you can handle the monthly payments.

Location is key

Before you start house hunting, be clear about where you want to live. Consider the neighborhood, the overall location, and what kind of property you need to save your own time and energy.

For instance, public education for students in grades 1 through 12 is free in the US, but it’s important to realize that taxes—of which real estate taxes make up the majority in localities—are used to fund these exemptions. There is a very solid rule of thumb that states or provinces with higher property values often means higher local taxes, better schools, healthcare, and more amenities because of that tax money.

That being said, while selecting real estate, you should consider the availability of hospital and school facilities in the neighborhood, especially if you have young kids. This may lead you to more expensive markets where you will have to settle for a smaller home in exchange for higher-quality public services.

Readjust to the market

You do not need to swing and run after the market, but adapt to it, and design your plan for what’s next to come.

The current real estate market is still “thawing” and may work against first-time homebuyers. The best thing you can do is to constantly have a fast, executable plan of action and be mentally ready to take advantage of the perfect chance.

Having a pre-approved mortgage from a reliable lender gives you an edge, even if you can’t be sure of winning every bid. Pre-approval shows sellers you’re ready to buy, with your finances checked and approved. Plus, it avoids surprises later and keeps the loan process smoother.

MARKET SPOTLIGHT: CATCH UP ON THE LOAN (updated December 26, 2023)

If you bought a house with today’s high mortgage rates, it could take you 13.5 years just to break even on your investment.

According to Zillow, some people in the US are choosing to buy homes despite high mortgage rates, not for immediate profit, because they see it as a long-term investment that will strengthen their financial future.

Traditionally, homeowners break even on their investment (meaning selling price covers costs) in 4-6 years. For some, especially first-time buyers, hearing it could take over a decade might be a surprise. Reaching break-even point is not about recouping costs for most homeowners. As Matt Dunbar, vice president of Churchill Mortgage explains, it’s a big milestone. It involves financial stability, growing equity, and freedom to pursue future financial goals.

Still, not all housing markets and not all buyers face a decades-long break-even threshold. The question of how long it takes to break even depends on many factors, such as your mortgage rate, down payment size, property taxes and how fast prices are rising in your area.

Deciding when to buy or sell is personal. It is up to personal budget, upcoming plans, and how comfortable you are with the payments.

Another update for you: owning a home in the US has gotten way pricier than renting lately. A report by CBRE Research found that monthly mortgage payments are now 52% more expensive than the average rent.

Soaring house prices make it tough for many renters to save up a 10% down payment, let alone cover monthly payments with interest rates shooting up. If buying becomes unrealistic for most, landlords might jack up rents even further, potentially hurting big investors who’ve heavily invested in US rental properties.

Reece Almond

Disclaimer: The blog articles are intended for educational and informational purposes only. Nothing in the content is designed to be legal or financial advice.