“Across the country, insurers are facing more bad years than good years. If this trend continues, it could destabilize the broader economy”, researchers and editors from New York Times said.

What’s happening?

To May 2024, data collected from Quadrant Information Services (QIS) shows that average cost of home insurance is around $2,151 every year, with a policy of $300k in dwelling coverage. But this number varies, depending on many other factors like where you live or which coverage limit you stick to. Along with QIS, Forbes briefed their analysis, so we have more idea of what is going around.

For example, states like Vermont, New Hampshire, and Delaware, homeowners can expect to pay less than $1,500 per year for policies with $300,000 in dwelling coverage. Yet Oklahoma and Nebraska can see costs surpassing $4,000 annually for similar coverage.

Sadly, home insurance rates across the US states have been shooting up, according to Realtor, where Texas, Colorado, Arizona and Utah saw the highest surge, exceeding 50% and Oklahoma experienced much lower increase of around 42%. By city cost, Los Angeles, Chicago, and Houston TX top the list, with an average monthly rate ranging from $154 to $414.

Why are these numbers? What do they tell?

We got a glimpse at those numbers. The next question is what do they further indicate?

First, the rising turmoil within the home insurance market is making it worse for homeowners who have always paid their premium and never made a claim. They face unexpected policy cancellations that force them to scramble for alternative coverage for their most significant asset – their homes.

Many are left with high-risk insurance pools backed by the state, which often offer inferior coverage compared to standard policies. Briefly, what we can say about the situation is: a lack of effective strategies from the government to toss back the stability to this market.

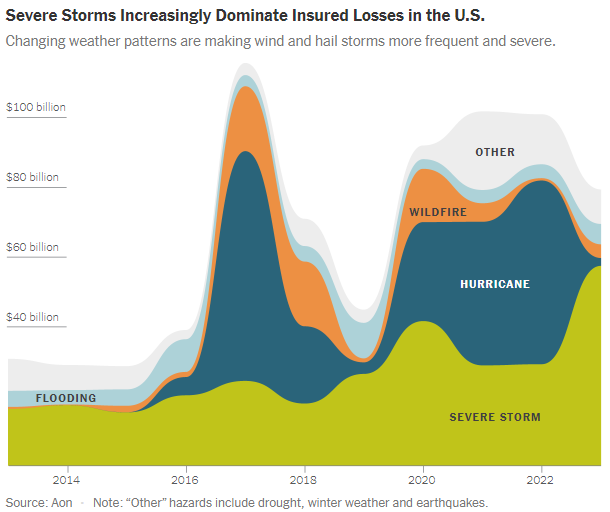

Second, the home insurance market changes and slowly crumbles due to the weather shifts. More polluted air, intense heat and storming sea waves are becoming less predictable, causing the fragility of home insurance segment more apparent and visible than ever.

That’s why most insurers “avoid” Florida, Louisiana due to its reputation for being a tough market. With their long coastline and narrow shape, they are more exposed to risks of heavy damage and constant flooding than any other state.

“Insurance is where many people are feeling the economic impacts of climate change first,” said Carolyn Kousky, said Environmental Defense Fund’s associate vice president for economics and policy to The New York Times. “That is going to spill over into housing markets, mortgage markets, and local economies.”

Home insurance woes are a domino effect threatening the American housing market. Without band-aids, banks won’t lend, home sales plummet, and property values tank. This cash crunch starves communities of tax revenue for schools, police, and essential services. It’s a problem, everybody knows, but not everyone sees the next feasible action.

Finally, we scroll back to the all-time question whether as a real estate investor, this shifted home insurance market is a more suitable time to buy a completely new home or purchasing a vintage property.

Alright, while new builds boast lower upfront maintenance, established properties offer unique advantages that new construction simply can’t replicate. Why? Sign up for our “Deal of the Day” to see why pre-foreclosure deals can be your best unlisted established properties with the most profitable equity and discount. It’s all on the house, so step up, and let us be a part of your investing story.

Reece Almond

Disclaimer: The blog articles are intended for educational and informational purposes only. Nothing in the content is designed to be legal or financial advice.